What if the very property you think is your retirement nest egg is actually the anchor keeping you from real wealth? Most Singaporean investors are currently trapped in a cycle of low rental yields, watching their capital sit idle because they haven’t mastered the quadrant framework. You likely feel the sting of the 20% ABSD on your second property or the fear of making a S$100,000 mistake in an unfamiliar industrial niche. It’s a common frustration to own an asset yet still feel chained to your desk to pay the bills.

This guide changes that. You’ll learn how to apply this strategic model to transition from a single-unit owner into a sophisticated portfolio investor. We’ll show you the exact steps to diversify into high-yield co-living and industrial spaces that generate consistent positive cash flow even in the 2026 market. We’re moving past abstract theory to give you a proven blueprint for financial freedom, helping you trade your “employee” mindset for the strategic precision of a seasoned pro.

Key Takeaways

- Stop settling for mediocre returns and discover how the property investment quadrant serves as your map to transition from a single-unit owner to a high-yield portfolio investor.

- Identify whether you are currently an “Accidental Landlord” and learn the specific tactics required to evolve into a strategic “Yield Hunter” for maximum occupancy.

- Navigate the “ABSD Wall” and optimize your CPF usage to ensure your mortgage strategy generates positive cash flow instead of draining your reserves.

- Audit your existing holdings for “dead equity” and learn how to optimize residential assets through proven co-living and refurbishment models.

- Master a results-driven blueprint that moves you beyond theory and into real-world application for a scalable, high-performance property portfolio in Singapore.

What is the Property Investment Quadrant in the Singapore Context?

Stop viewing real estate as just a roof over your head or a lucky strike in the resale market. The Property Investment Quadrant is a rigorous framework designed to classify how you generate wealth. It moves you away from the “buy-and-hope” mentality. In the Singaporean market, this framework distinguishes between those who work for their properties and those whose properties work for them. While many rely on the traditional residential buy-and-hold strategy, that approach is only a tiny slice of the map. You need to understand real estate investing principles to see that true wealth isn’t found in waiting 20 years for a price surge. It’s found in monthly cash flow.

The 2026 market demands a shift from being an “Active Landlord” to becoming a “Passive Portfolio Owner.” An active landlord chases tenants and fixes toilets; a passive owner builds a system. This is where the I Quadrant becomes essential. It applies specifically to our local regulatory environment, helping you navigate cooling measures and financing limits. You don’t just buy a unit; you acquire an asset that fits into a larger, cash-generating engine.

The Evolution of the Quadrant for 2026 Investors

The days of easy property flipping ended when Additional Buyer’s Stamp Duty (ABSD) rates hit 20% for a Singaporean’s second property and 30% for the third. These high entry barriers have redefined the “Investor” quadrant. You can’t rely on short-term capital gains to cover these costs anymore. Success in 2026 requires a sophisticated focus on high-yield niches like co-living or industrial spaces. The Property Quadrant is a strategic framework that prioritizes generating immediate, consistent monthly cash flow over the speculative hope of long-term capital appreciation. Master this shift, and you unlock the ability to scale despite cooling measures.

Why Most Singaporeans are Stuck in the Wrong Quadrant

Most Singaporeans are trapped in a psychological cage. They view their primary residence as their biggest investment, but a home you live in is a liability that takes money out of your pocket every month. This mindset fuels the rat race because it lacks a clear path for asset progression. You’re working for the bank, not for your freedom.

There is a massive difference between owning a property and owning a property business. Owning a property makes you a hobbyist; owning a business means you’ve mastered the quadrant. It means you’ve implemented systems to ensure 95% occupancy and positive cash flow regardless of market sentiment. If you want to stop trading your time for a paycheck, you must stop acting like a homeowner and start acting like a portfolio strategist. Use the framework to identify where your money is currently sitting and move it into assets that pay you to own them.

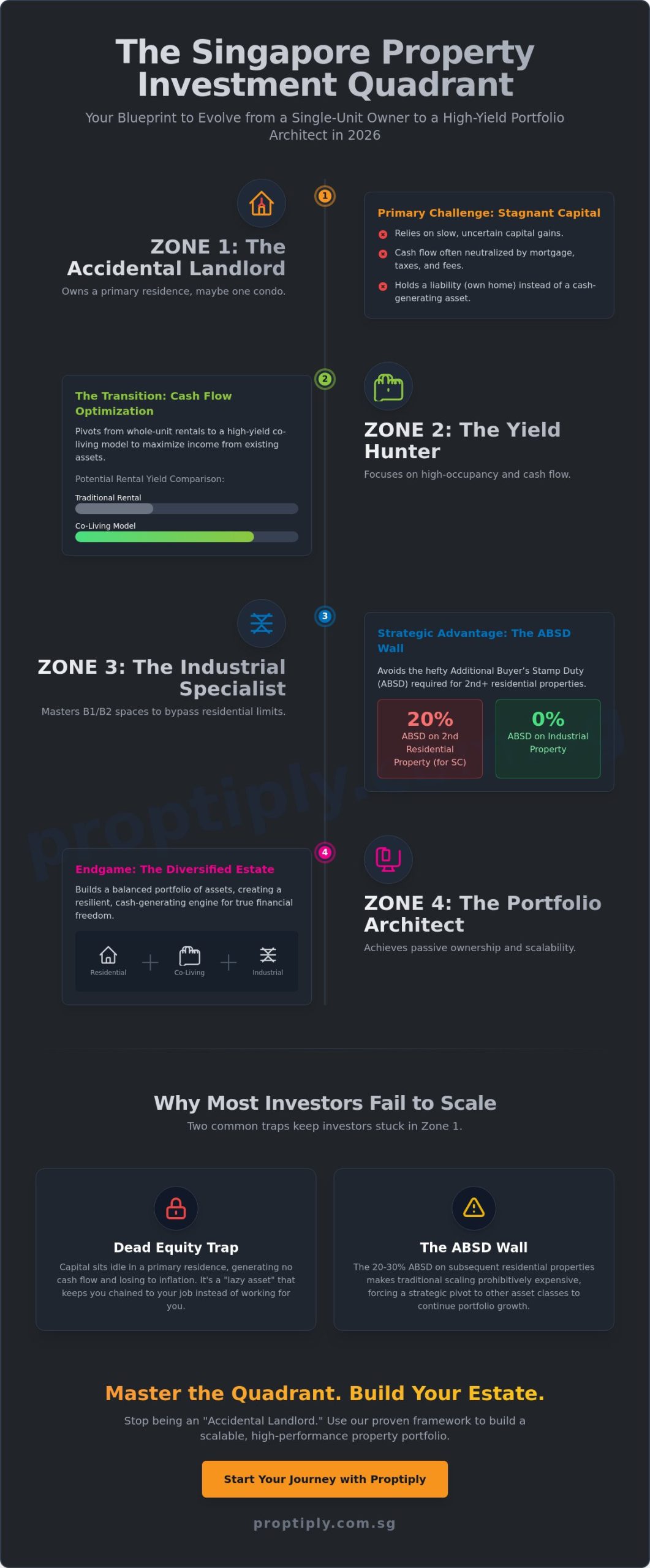

The Four Zones of the Singapore Property Quadrant: Where Do You Stand?

To scale your wealth in 2026, you must first identify your current position within the property quadrant. Most Singaporeans begin as Zone 1 “Accidental Landlords.” These are individuals who own a primary residence and perhaps one investment condo, often relying on high leverage and hoping for capital gains. Zone 2 “Yield Hunters” take it a step further by focusing on high-occupancy strategies like co-living to generate immediate cash flow. Zone 3 “Industrial Specialists” pivot away from residential constraints to master B1 and B2 spaces. Finally, Zone 4 “Portfolio Architects” build a diversified estate that balances risk and reward across multiple asset classes.

Zone 1 & 2: Mastering the Residential and Co-living Niche

Your first HDB or private condo is merely the entry point to the quadrant. It’s a foundation, but it’s rarely enough to achieve financial freedom. In Zone 1, investors often find their cash flow neutralized by high interest rates or maintenance fees. To break through to Zone 2, you must optimize your existing assets. This is where co living singapore strategies become a game changer. By pivoting from traditional whole-unit rentals to room-based rentals, you can effectively double your rental income without the need to acquire additional titles.

The secret to moving from Zone 1 to Zone 2 lies in professional tenancy management. You’ve got to stop viewing yourself as a passive owner and start acting like a boutique operator. Efficiently managing tenant mix and utility costs ensures your yield remains robust even when the wider market fluctuates. It’s about maximizing the “rentable per square foot” metric to ensure every cent of your mortgage works for you.

Zone 3 & 4: Transitioning to Commercial and Industrial Assets

When residential cooling measures like the 20% Additional Buyer’s Stamp Duty (ABSD) on a second property begin to stifle your growth, it’s time to look toward Zone 3. Industrial B1 and B2 properties offer a “hidden” escape for the savvy investor. These assets currently carry no ABSD and frequently offer gross yields between 5% and 7%, significantly outperforming the 2% to 3% typically seen in the residential sector. Smart investors align these acquisitions with Singapore’s long-term development plans to ensure they buy in high-growth corridors.

Understanding the business park and industrial segments provides a vital layer of stability. These spaces cater to corporate tenants who often sign longer leases, providing a predictable income stream that residential assets sometimes lack. The ultimate goal for a Zone 4 Portfolio Architect is a self-sustaining system. This involves using GST-registered entities to manage tax efficiencies and holding a mix of assets that survive different market cycles. If you’re feeling stuck at your current level, it might be time to refine your strategy with a proven framework.

Why Most Investors Fail to Scale Across the Quadrant

Many Singaporeans dream of building a multi-property empire, yet most never move past their first investment unit. They hit an invisible ceiling. The ABSD Wall is the primary culprit, with current 2026 tax rates for second and third properties making traditional residential flipping nearly impossible for the average earner. Without a clear strategy to navigate this quadrant, your capital stays locked in a single asset while inflation erodes your purchasing power.

Another silent killer is the “CPF Trap.” You might think using CPF for mortgage payments is smart because it preserves your cash. In reality, this often leads to negative cash flow when you factor in the accrued interest you owe back to your Ordinary Account. If your property isn’t generating actual cash in hand every month, you aren’t an investor; you’re just a glorified saver. Poor property management in Singapore further compounds this, as DIY landlords lose thousands to tenant disputes, maintenance delays, and prolonged vacancies that eat into net returns.

The biggest psychological barrier is the fear of commercial and industrial spaces. Investors often label these as “too risky,” despite the Singapore property market resilience shown in non-residential sectors. While residential buyers struggle with cooling measures, savvy players use industrial assets to bypass ABSD entirely and secure higher yields.

The TDSR and MSR Hurdles in 2026

Your ability to move within the quadrant depends entirely on your borrowing capacity. Total Debt Servicing Ratio (TDSR) remains a strict gatekeeper in 2026, ensuring you don’t overleverage. Master the art of “decoupling” to legally free up one name for a second property purchase without incurring heavy taxes. This requires precise timing and legal expertise. Don’t guess your numbers. A 1-on-1 portfolio consultation is the only way to verify your current standing before you commit to a new loan.

The Risk of the “Single Asset” Trap

Concentrating 100% of your wealth in one residential unit is a recipe for stagnation. It’s helpful to look at the automotive market to understand this logic. A car is a depreciating liability that drains cash, while a diversified property portfolio is a vehicle for growth. Diversification across different asset classes is the only way to reach the “I” (Investor) quadrant where money works for you. Stop putting all your eggs in one HDB or condo basket and start looking at high-yield industrial niches to balance your risk profile.

How to Move Across the Quadrant: A Step-by-Step Scaling Strategy

Scaling a portfolio in the 2026 Singapore market requires more than just capital. It demands a systematic transition through the investment quadrant. Most investors get stuck because they treat their first property as a trophy rather than a tool. To break free, you must treat your holdings as a business. Follow this five step blueprint to accelerate your progression.

- Step 1: Audit for dead equity. Calculate the trapped value in your current home. If your property has appreciated by S$300,000 over ten years but your rental yield is stagnant, that capital is underperforming.

- Step 2: Optimize through co-living. Don’t settle for traditional tenancies. Refurbish residential units into co-living spaces to boost gross yields from a standard 2.5% to 6% or higher.

- Step 3: Pivot to commercial niches. Use industrial assets to bypass the 20% or 30% ABSD rates that cripple residential scaling.

- Step 4: Reinvest every cent. Avoid lifestyle inflation. Funnel your positive cash flow back into your next down payment.

- Step 5: Master the craft. Attend specialized bootcamps to learn the “boots on the ground” tactics that general agents won’t tell you.

Auditing Your Current Assets

Your “Return on Equity” (ROE) is the only metric that matters. To find it, divide your annual net gain (rental profit plus principal reduction) by your current home equity. If your ROE is lower than 4%, you’re losing money to inflation. Many HDB owners wait too long to sell, missing the window where their flat hits its peak valuation. Use the 2025 URA Master Plan updates to identify high-growth zones like the Jurong Lake District or the Greater Southern Waterfront. Moving your capital from a stagnant heartland estate into a growth quadrant can double your net worth within a single five year cycle. For HDB flat owners evaluating their asset progression timeline, understanding the investment impact of the october BTO 2024 launch and its 2026 retrospective provides critical context on how new supply and the extended Minimum Occupation Period affect your resale exit strategy.

Executing the Move to Industrial and Commercial

Industrial property is the “secret sauce” for Singaporean investors in 2026. You must understand the distinction between B1 and B2 zones. B1 properties are for clean and light industries like software development or telecommunications. These are easier to manage and often located closer to MRT stations. B2 zones allow for heavy industry and can offer higher yields, though they require more robust maintenance.

Smart investors use a GST-registered company for these acquisitions. This allows you to claim back the 9% GST on the purchase price, significantly lowering your initial capital outlay. When looking for tenants, target recession-proof sectors like e-commerce logistics or food processing. These businesses prioritize long-term leases, providing the stability you need to fund your next residential play. For investors who want to understand how to evaluate a specific residential project before making this kind of strategic pivot, the Midwood condo investment blueprint offers a repeatable framework for calculating real-world yields and identifying high-growth OCR opportunities.

Stop guessing and start executing with a proven framework. Join our next property wealth masterclass to see how we build high-yield portfolios from scratch.

Master the Quadrant with Proptiply’s Proven Framework

Theory alone won’t build a legacy. You can study every property book on the shelf, but the Singapore market moves on data and policy, not just ideas. To truly master the property quadrant, you need a blueprint that accounts for the specific economic climate of 2026. Our framework bridges the gap between abstract knowledge and the “boots-on-the-ground” reality of local real estate. We focus on what actually works in a high-interest, high-ABSD environment.

Our Residential Acceleration Program helps you navigate the first half of the investment quadrant with precision. We don’t just talk about buying low; we show you how to identify undervalued private properties that fit your specific debt-to-income ratio. For a typical Singaporean couple with a combined monthly income of S$15,000, we provide the exact steps to transition from a single HDB to a multi-property portfolio without over-leveraging. We prioritize asset progression that complies with the latest MAS framework while maximizing capital appreciation. A case study like the Midwood condo analysis for Singapore property investors illustrates exactly how to apply this entry-price discipline to a real suburban project before committing your capital.

Scaling to a professional level requires a shift in strategy. This is where our Commercial and Industrial Program (CAIP) becomes your greatest asset. While residential yields often hover around 2.5%, industrial spaces can offer gross yields of 5.5% or higher. We teach you how to navigate these specialized sectors to build a resilient, high-cash-flow portfolio that isn’t hit by the same restrictive cooling measures found in the residential market. It’s about moving from being an accidental landlord to a strategic asset manager.

The Proptiply Advantage: From Education to Execution

We operate as a community of practitioners, not a classroom of theorists. Our co-living bootcamp provides an immediate tactical advantage by showing you how to maximize rental yield through strategic space planning. Some of our graduates have seen rental income spikes of over 40% by implementing our specific co-living models. We’ve watched countless students move from the “Employee” mindset to becoming “Professional Investors” by following our disciplined, results-driven methodology. You’ll learn from people who are actively buying, managing, and flipping properties in today’s market.

Your Next Step to Financial Freedom

The 2026 market window offers a unique set of opportunities for those prepared to act. Stop dreaming. Stop letting “analysis paralysis” stall your progress. It’s time to apply a systematic framework to your wealth creation. Your financial freedom depends on the actions you take today, not the plans you make for next year. Don’t let another market cycle pass you by while you sit on the sidelines. Take the first step toward a secure, passive income stream now.

Secure Your Path to Passive Income Today

Scaling your property portfolio in the 2026 Singapore market requires more than just capital; it demands a systematic approach to asset progression. You’ve now seen how identifying your current position within the property quadrant is the essential first step toward unlocking consistent positive cash flow. By strategically transitioning from traditional residential units into high-yield niches like co-living or industrial spaces, you can bypass the common pitfalls that stall most local investors. Success isn’t about luck. It’s about the disciplined application of a proven framework.

Since 2016, Proptiply has empowered investors with over a decade of deep market expertise. Led by active practitioners Jelene Lum and Ervin Ang, our specialized bootcamps for Residential, Commercial, and Co-living niches provide the granular, boots-on-the-ground detail needed to avoid expensive mistakes. You don’t have to navigate these complexities alone. Take the next step toward financial freedom by leveraging our insider knowledge and real-world tactics.

Master the Quadrant and build your wealth roadmap with a Proptiply 1-on-1 Consultation

Your journey toward a secure financial legacy starts with a single, decisive action. We’re ready to help you unlock your full investment potential and build a future you can be proud of.

Frequently Asked Questions

What is the “I Quadrant” in Singapore property investing?

The “I Quadrant” refers to the Investor Quadrant, a specialized strategic framework designed to shift your mindset from passive homeownership to active wealth creation. It’s the stage where you stop working for your property and start making your property work for you. By mastering this quadrant, you transition into high-yield assets like industrial spaces or co-living units that generate consistent positive cash flow. This methodology moves you beyond the 2% yields of traditional residential units into more lucrative territory.

How can I avoid ABSD when scaling my property portfolio in 2026?

You can legally avoid Additional Buyer’s Stamp Duty (ABSD) by pivoting your investment strategy toward the commercial and industrial property sectors. Under current IRAS regulations, ABSD only applies to residential properties. By diversifying into the industrial quadrant, you save up to 20% or more in taxes on your second or third property purchase. This allows you to deploy 100% of your capital into the asset itself rather than paying hefty government levies. It’s a proven blueprint for scaling fast.

Is industrial property a better investment than residential in Singapore?

Industrial property often outperforms residential units because it typically offers gross yields of 5% to 7%, compared to the 2% to 3% seen in the residential market. These assets also benefit from shorter lease cycles and lower maintenance costs. While residential properties rely heavily on speculative capital appreciation, industrial investments prioritize immediate positive cash flow. In 2024, JTC data showed industrial rents remained resilient, making them a more stable choice for investors seeking monthly income over long-term bets.

Can I use my CPF to invest in the commercial or industrial quadrants?

You cannot use your CPF Ordinary Account (OA) funds to purchase industrial or commercial properties directly. CPF usage is strictly reserved for residential properties or specific approved investment schemes. This means you need to prepare sufficient cash reserves for the down payment and monthly mortgage of a commercial unit. However, this limitation is actually a filter that reduces competition from retail buyers. It keeps the market professional and ensures that only serious investors who understand the quadrant strategy are participating.

How much capital do I need to move from the residential to the commercial quadrant?

You typically need a minimum cash outlay of S$200,000 to S$350,000 to secure a mid-sized industrial unit in the current market. This covers the 20% to 30% down payment required by banks for non-residential loans, plus legal fees and GST. Since you can’t use CPF, your cash liquidity is vital. Many successful Proptiply students start with smaller B1 industrial spaces to build their momentum. This entry point allows you to test the waters before scaling into larger, more complex commercial assets.

What are the risks of the co-living investment strategy in Singapore?

The primary risks of co-living include sudden regulatory shifts from the URA and higher tenant turnover rates. If you don’t manage the property efficiently, vacancy periods can quickly eat into your profits. You must also adhere strictly to the 6-occupant rule for private residential properties to avoid heavy fines or legal action. Mitigate these risks by implementing a systematic management framework and choosing locations near MRT stations. Our proven co-living blueprint helps you navigate these pitfalls with ease.

How does the 2026 URA Master Plan affect my quadrant strategy?

The 2026 URA Master Plan identifies specific high-growth regions like the Jurong Innovation District and the Punggol Digital District for massive infrastructure development. These areas are prime targets for your industrial quadrant strategy because they attract high-value tenants and promise long-term capital appreciation. By aligning your purchases with government decentralization efforts, you ensure your portfolio remains relevant and high-yielding. Always cross-reference your investment picks with the latest URA zoning maps to maximize your success rate and avoid stagnant areas.

Why is a property investment course necessary if I already own a home?

Owning a home is about shelter, but property investment is about financial engineering and risk management. A structured course provides the technical knowledge you won’t get from just living in a flat, such as calculating net yields or understanding industrial JTC land tenures. It helps you avoid the S$100,000 mistakes that many unguided buyers make when entering the commercial space. You’ll gain access to an exclusive community and insider knowledge that turns a simple home into a scalable, wealth-generating engine.