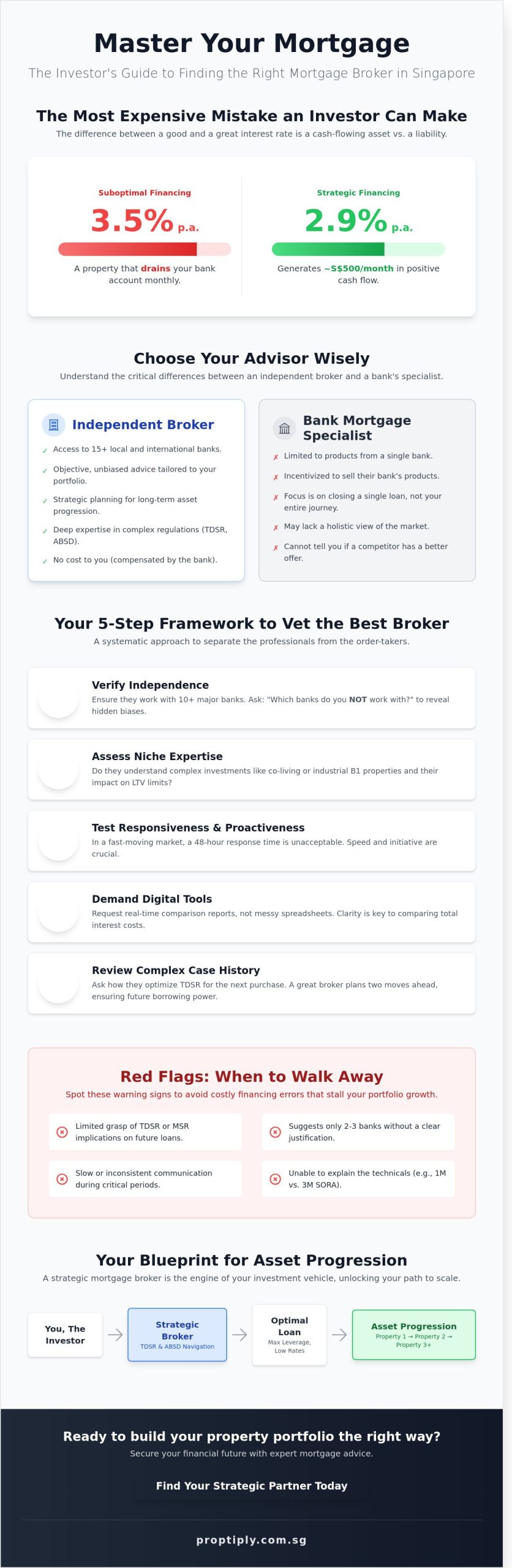

The most expensive mistake a Singapore investor can make isn’t overpaying for a unit; it’s securing the wrong financing structure. In 2024, the gap between a 3.5% and a 2.9% interest rate can mean the difference between S$500 in monthly positive cash flow and a property that quietly drains your bank account. To scale your portfolio effectively, you must find a mortgage broker who acts as a strategic architect rather than a simple paper-pusher.

It’s natural to feel overwhelmed by the technical shift from LIBOR to SORA or the fear that your next application will hit a TDSR wall. You deserve to know if your broker is truly independent or just chasing a bank commission. This guide will help you master the art of selecting a mortgage partner who unlocks asset progression and maximizes your rental yield. We’re sharing the exact framework to secure the lowest rates and maximize your borrowing capacity for a hassle-free application process.

Key Takeaways

- Understand how a strategic broker serves as a vital intermediary to 15+ banks, helping you navigate complex cooling measures like ABSD and TDSR.

- Master a proven 5-step framework to find a mortgage broker who possesses the niche expertise required for high-yield co-living and industrial investments.

- Compare the benefits of independent brokers versus bank specialists to ensure you gain “multi-brand” access and objective advice at no cost to you.

- Spot critical red flags early, such as a limited grasp of MSR or TDSR, to avoid costly financing errors that can stall your asset progression.

- Learn to integrate your mortgage partner into a broader investment blueprint that prioritizes positive cash flow and long-term wealth creation.

Why Finding the Right Mortgage Broker is Critical for Singapore Investors

Stop thinking like a consumer. Think like a wealth builder. To succeed in the competitive Singapore property market, you must understand what a mortgage broker is and how they serve as a strategic intermediary. They don’t just find you a loan; they manage your relationship across 15+ major banks. While a typical home buyer focuses solely on the lowest interest rate, a seasoned investor focuses on leverage, liquidity, and long-term cash flow. The right financing structure is what turns a standard residential unit into a high-yield co-living space or a profitable industrial asset.

When you decide to find a mortgage broker, you’re hiring a navigator for Singapore’s complex cooling measures. Between the 60% Total Debt Servicing Ratio (TDSR) and the tiered Additional Buyer’s Stamp Duty (ABSD), one wrong move can freeze your capital for years. A broker understands that financing is the engine of your investment. If the engine is tuned correctly, you achieve positive cash flow. If it’s not, you’re stuck with an underperforming asset that drains your monthly savings.

The “Asset Progression” Advantage

Smart investing isn’t about the first property. It’s about the third and the fourth. A broker helps you plan your next move before you even commit to your current purchase. They specialize in loan structures that facilitate decoupling strategies, allowing couples to free up one name for a second property without hitting the ABSD wall. This forward-thinking approach is a pillar of our real estate investment advice. If your loan isn’t structured for progression, your roadmap to financial freedom hits a dead end before you’ve even started.

Understanding Singapore’s Lending Landscape in 2026

The lending environment in 2026 is defined by SORA-pegged rates and shifting MAS regulations. You need to know exactly when to choose a fixed rate for stability or a floating rate to capture downward trends. Going direct to a bank is often a trap for the uninformed. A bank officer only sells their own products. They won’t tell you if a competitor offers better terms for B1 industrial spaces or higher LTV limits for your specific profile. To truly find a mortgage broker who adds value, look for someone who understands how TDSR affects your future borrowing power. They ensure your current debt doesn’t disqualify you from future opportunities.

A 5-Step Framework to Find and Vet a Mortgage Broker

Don’t leave your financial future to chance. To find a mortgage broker who actually adds value to your portfolio, you need a systematic approach. Follow this 5-step framework to separate the professionals from the order-takers.

- Step 1: Verify independence. Ensure they work with all 10+ major local and international banks in Singapore. If a broker only suggests three options, they aren’t searching for the best deal; they’re searching for the easiest commission.

- Step 2: Assess niche expertise. Generalists struggle with specialized investments. If you’re targeting co-living spaces or industrial B1 properties, your broker must understand how these assets fit into your LTV (Loan-to-Value) limits.

- Step 3: Test responsiveness. In a fast-moving market, timing is everything. A broker who takes 48 hours to reply to a WhatsApp message will cost you money when interest rates pivot. Look for “pro-activeness” and speed.

- Step 4: Demand digital tools. You need clarity, not messy spreadsheets. A top-tier broker provides real-time comparison reports that break down monthly installments and total interest costs over the lock-in period.

- Step 5: Review complex case history. Ask about their experience with self-employed individuals or multi-property owners. Navigating the 55% Total Debt Servicing Ratio (TDSR) requires a strategist, not just a messenger.

Questions Every Investor Should Ask

Put your potential broker in the hot seat. Start by asking: “Which banks do you NOT work with?” The answer reveals hidden biases immediately. Follow up with: “How do you help me optimize my TDSR for my next purchase?” A great broker plans two moves ahead, ensuring your current loan doesn’t block your next acquisition. Finally, ask for their view on the current 3-month SORA vs 1-month SORA. Their technical depth here shows whether they truly understand the mechanics of Singapore’s housing loan regulations and how they impact your cash flow.

Verifying Credentials and MAS Status

Your financial data is private. Before sharing your Notice of Assessment (NOA) or CPF statements, verify the broker’s firm is properly registered and compliant with MAS guidelines. Data privacy isn’t negotiable. You should also have a transparent conversation about fees. In Singapore, most residential mortgage brokers are compensated by the banks, making their service free for the borrower. If there are any administrative charges or “consultancy fees,” they must disclose these in writing before you sign any documents. Protecting your capital starts with mastering property investment fundamentals, and that includes vetting your inner circle of advisors.

Independent Broker vs. Bank Mortgage Specialist: A Comparison

A bank mortgage specialist sells you one thing: their own bank’s product. It is a “one-brand” shop. If their current fixed rate is 3.5%, that is what you get, even if a competitor across the street offers 3.1%. When you decide to find a mortgage broker, you gain access to 150+ loan packages from across the entire Singapore market. This multi-brand access is the bedrock of smart asset progression. It ensures you don’t leave money on the table.

Brokers work on a commission model where the bank pays them, not you. This fee structure does not compromise objectivity. A reputable broker wants your repeat business for your future portfolios, so they focus on the numbers that maximize your cash flow. You should avoid the “loyal customer” trap at all costs. Many Singaporeans believe their primary bank will reward a 10-year relationship with a lower rate. In reality, banks often reserve their best acquisition rates for new customers. Staying loyal without comparing the market is a fast way to lose S$2,000 to S$5,000 in interest every single year.

When to Go Direct to a Bank

Go direct if you hold high-tier priority banking status, where you can negotiate bespoke rates unavailable to the general public. Sometimes, a bank launches an internal flash sale promotion that brokers cannot access for the first 48 hours. Even in these cases, successful investors get a second opinion from a broker. This validates whether that bespoke rate actually beats the broader market average or is just clever marketing.

The Broker’s Role in Post-Purchase Support

Securing the loan is only the first step in the blueprint. A broker acts as your protective guide during the critical Option to Purchase (OTP) stage. They ensure your Letter of Offer is signed before the 14 to 21 day deadline expires. Missing this timeline can lead to a forfeited deposit, an expensive mistake that can derail your investment journey.

Your broker also tracks the second and third year traps. Most Singapore home loans feature teaser rates that spike after 36 months. A professional broker monitors this window and prompts you to reprice or refinance six months before the hike hits. They handle the heavy lifting, from coordinating with law firms for conveyancing to managing valuation reports. This level of support allows you to focus on scaling your property portfolio while they manage the technical paperwork.

Red Flags: When to Walk Away from a Mortgage Advisor

Don’t settle for mediocrity when you attempt to find a mortgage broker. An amateur advisor doesn’t just provide bad service; they can actively destroy your path to financial freedom. You need a strategist who understands the blueprint of wealth creation, not a salesperson chasing a quick check. If you spot these warning signs, walk away immediately to protect your capital.

- Limited Bank Options: A professional broker should have access to over 10 different lending institutions. If they consistently push only one or two banks, they’re likely prioritizing their own commission structures over your interest savings.

- Regulatory Confusion: Total Debt Servicing Ratio (TDSR) is currently capped at 55% for private properties, while Mortgage Servicing Ratio (MSR) stands at 30% for HDB flats. If an advisor fumbles these calculations, they’ll lead you into a rejected application.

- OTP Pressure: Never sign an Option to Purchase (OTP) before your In-Principle Approval (IPA) is firm. A broker who pressures you to commit without an IPA is asking you to gamble your 1% option fee, which can be S$10,000 or more on a typical private property.

- Rental Income Ignorance: To recognize 70% of rental income for your next loan, your tenancy agreement singapore must meet specific IRAS and bank requirements. If they don’t understand how to leverage these documents, your borrowing power will remain stagnant.

The Danger of the “Pushy” Broker

Strategy-driven advice focuses on your five-year exit plan. Commission-driven advice only cares about the current month. You can spot the difference by how they handle the “lowest rate” pitch. A 1.5% rate sounds great, but it’s a trap if it comes with a three-year lock-in period and you plan to sell in two. Protect your personal data. A professional never “blasts” your NRIC and income docs to every bank at once. This desperate tactic can negatively impact your credit score and signal risk to lenders.

Technical Gaps to Watch For

An expert must explain the nuances between Building Under Construction (BUC) progressive payments and completed property loans. If you’re exploring industrial property investment, ask about GST financing. Many beginners are shocked by the cash outlay for GST on a S$1.5 million unit. Your broker should also advise on the strategic use of CPF versus cash. Relying too heavily on CPF can lead to high accrued interest, which eats into your eventual cash proceeds when you sell. Demand a broker who offers a clear, data-backed plan for your asset progression.

Building Your Investment Blueprint with the Right Partners

Securing a loan is a tactical victory, but it isn’t a strategy. While you now know how to find a mortgage broker who can navigate the latest MAS regulations, remember that a broker is just one specialized technician in your wealth-building team. They provide the tools, but you must provide the blueprint. Without a clear “why” behind every acquisition, even the most competitive interest rate in Singapore won’t protect you from a stagnant portfolio. You need to lead your broker with a specific mandate based on your long-term financial goals.

Mastering the Financing Game

Proptiply bootcamps empower you to take the driver’s seat by teaching you the mechanics of high-yield investing. We move beyond basic loan comparisons to focus on the numbers that drive real wealth. You’ll learn to calculate Return on Investment (ROI) and Cash-on-Cash (CoC) returns with the precision of a seasoned pro. These metrics are your north star when evaluating whether a property deserves a spot in your portfolio.

Your financing requirements will shift dramatically as you scale. Moving from residential units to industrial properties involves a completely different set of rules, including GST considerations and different Loan-to-Value (LTV) limits. We’ve navigated these transitions ourselves and show you how to prepare your finances for each stage of asset progression. Positive cash flow is the ultimate goal of strategic financing where your monthly rental income exceeds every single ownership expense including mortgage repayments, taxes, and maintenance fees.

Next Steps: Get Your Portfolio Roadmapped

Success in the Singapore property market isn’t about luck; it’s about the disciplined application of proven frameworks. We invite you to attend a Proptiply bootcamp to see these real-world strategies in action. You’ll see how we identify “hidden gem” industrial spaces and co-living opportunities that generate consistent passive income. This isn’t abstract theory. It’s the exact methodology we use to build and protect our own wealth.

A bespoke investment roadmap is the difference between a random collection of properties and a streamlined wealth engine. It gives you the clarity to walk into any bank or find a mortgage broker with total confidence in your numbers. Don’t just hunt for a loan; build a strategy that makes the loan work for you. Book a 1-on-1 Property Portfolio Consultation with Proptiply today to start designing your path to financial freedom. Let’s turn your investment aspirations into a concrete, actionable reality.

Secure Your Financial Blueprint Today

Securing the right financing is the engine behind every successful property portfolio in Singapore. You’ve learned that a broker isn’t just a middleman; they’re a strategic partner who helps you navigate TDSR limits and unlock better leverage. When you set out to find a mortgage broker, prioritize independence and niche expertise over generic bank offers. This ensures you avoid common pitfalls like restrictive lock-in periods or high-interest traps that eat into your rental yields.

Don’t leave your asset progression to chance. Our team has already trained over 1,000 students in Singapore, specializing in high-yield niches like co-living and industrial spaces. Led by active practitioners Jelene Lum and Ervin Ang, we focus on real-world application rather than abstract theory. It’s time to stop guessing and start implementing a proven framework for financial freedom. You have the tools to build a portfolio that lasts.

Master your property financing strategy at our next Residential Acceleration Program

Frequently Asked Questions

Is it really free to use a mortgage broker in Singapore?

Yes, it is completely free for you because mortgage brokers earn their commission directly from the banks once your loan is successfully disbursed. You won’t pay a single cent in service fees to find a mortgage broker who can compare rates across 15 plus banks in Singapore. This setup ensures you get professional advice without adding to your property acquisition costs.

Can a mortgage broker help me if my TDSR is already very high?

A broker can definitely help you navigate the 55% Total Debt Servicing Ratio (TDSR) limit by identifying banks with different credit appetites or suggesting loan restructuring strategies. They understand how to optimize your debt profile to meet MAS requirements. While they can’t bypass the law, they can help you unlock hidden borrowing capacity through debt consolidation or pledging liquid assets as collateral.

What is the difference between a mortgage broker and a bank mortgage specialist?

The main difference is that a broker provides access to the entire market, while a bank specialist only sells their own institution’s products. A broker compares packages from UOB, DBS, OCBC, and foreign banks simultaneously to find the lowest spread. This saves you the time of visiting 10 different branches and ensures you don’t miss out on hidden promotional rates that aren’t advertised online.

How far in advance should I find a mortgage broker before buying a property?

You should contact a broker at least 3 to 6 months before you plan to sign an Option to Purchase (OTP). This lead time allows you to secure an In-Principle Approval (IPA), which is typically valid for 30 days. Having an IPA ensures you know your exact budget, preventing the loss of your 1% booking fee due to a sudden loan rejection later in the process.

Can a broker help with refinancing an existing HDB or Condo loan?

Yes, brokers specialize in refinancing both HDB bank loans and private condo loans to secure better interest rates. Most savvy homeowners refinance every 2 to 3 years once their lock-in period ends to avoid the reset to higher floating rates. Your broker will calculate the break-even point to ensure the interest savings outweigh any legal or valuation fees involved in the switch.

Will using a broker affect the interest rate the bank offers me?

Using a broker will never increase your interest rate; in fact, you often get access to exclusive below-the-line rates not advertised to the general public. Banks view brokers as a cost-effective distribution channel and pass those savings directly to you. When you find a mortgage broker, you’re tapping into their volume-based bargaining power to secure the most competitive spreads available in the current market.

What documents do I need to prepare for a broker to give me a quote?

You need your NRIC, the last 15 months of CPF Contribution History, and your latest Income Tax Notice of Assessment (NOA). Salaried employees should also prepare their last 3 months of payslips to verify current income. Having these digital copies ready allows a broker to generate a precise loan quote and credit assessment within 24 to 48 hours.

Can a broker help with commercial or industrial property loans?

Yes, brokers are essential for commercial and industrial property loans where TDSR rules differ and GST considerations apply. They help you navigate the complexities of 60-year or 99-year leasehold industrial units, which often have stricter Loan-to-Value (LTV) limits. A broker’s expertise is vital for investors looking to scale their portfolios into high-yield commercial assets without hitting financial roadblocks.