Last Tuesday, Julian discovered how quickly a property dream can sour when he nearly lost his S$6,500 deposit because he didn’t understand the legal weight of the option to purchase before his bank loan was finalized. It’s a high-stakes moment when you’re handed that document; one wrong move can turn your strategy for asset progression into an expensive mistake. You probably feel that same underlying tension, worrying about losing your 1% fee or getting confused by the differing regulations for HDB and private properties. We’ve seen these fears stop many promising investors in their tracks, but it doesn’t have to be that way.

This article is your professional blueprint to master the legal mechanics of property acquisition and secure your next Singapore deal with absolute certainty. We’re stripping away the jargon to give you the same “boots-on-the-ground” tactics we use to protect our own capital. You’ll get a clear 21-day timeline of the process, a breakdown of your financial obligations at every stage, and the exact steps to take to avoid bank loan rejection. Let’s ensure you have the tools to move from curiosity to action without the stress.

Key Takeaways

- Master the legal mechanics of the option to purchase to secure an exclusive right to your target property and prevent other buyers from outbidding you.

- Navigate the distinct regulatory landscapes of HDB and private property transactions to ensure your contracts are compliant and your interests are protected.

- Avoid costly pitfalls by understanding the financial and legal consequences of non-exercise, including how to safeguard your initial option fee.

- Follow a clear, step-by-step roadmap from the initial viewing to the final exercise, ensuring a seamless transition from prospect to property owner.

- Shift from a homebuyer to an investor mindset to identify undervalued deals and apply a proven framework for building a high-yield portfolio.

What is an Option to Purchase (OTP) in the Singapore Context?

An option to purchase is a legally binding agreement that secures your right to buy a property. Think of it as a “reservation” document. The seller (grantor) gives you (the grantee) the exclusive right to buy the property at a fixed price within a specific timeframe, usually 14 to 21 days for private property. During this period, the seller is legally prohibited from offering the unit to anyone else. They can’t entertain higher offers or back out without legal consequences. This exclusivity gives you the breathing room to finalize your financing and perform due diligence without the fear of being “gazumped.”

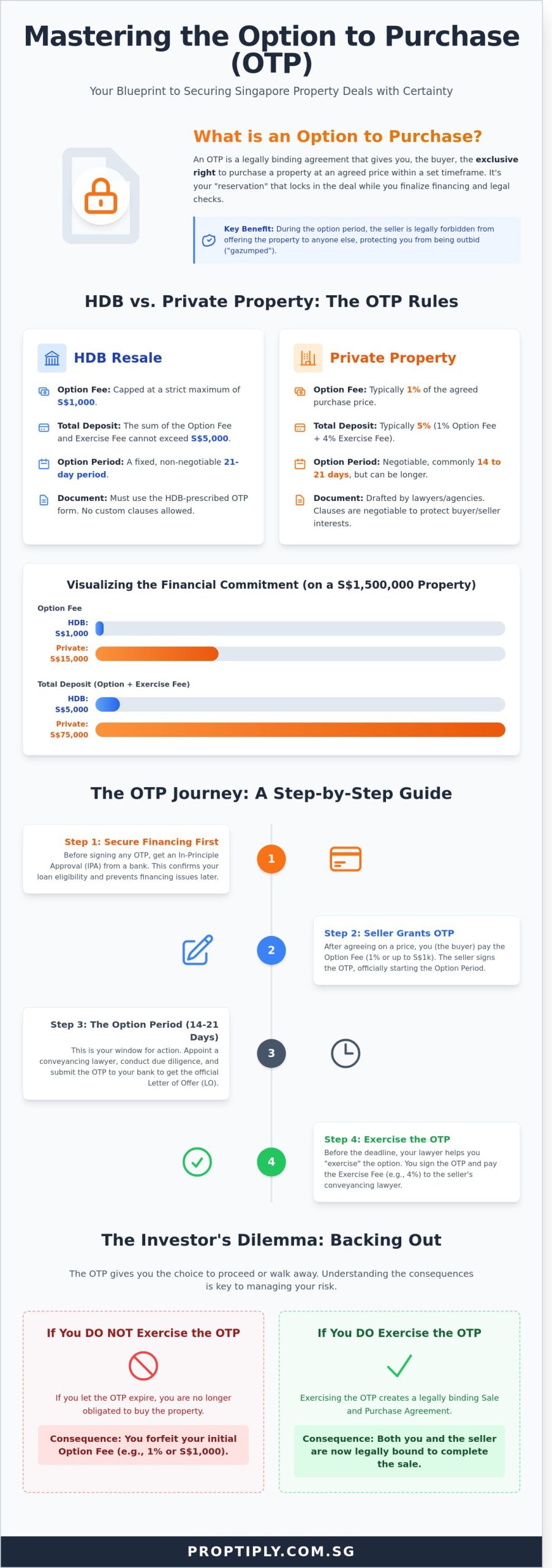

The process begins with the Option Fee. For private residential properties, this is typically 1% of the agreed purchase price. If you’re looking at public housing in Singapore, the rules are even more specific. HDB regulations cap the Option Fee at a maximum of S$1,000. This document is the most critical piece of paper in your early investment journey. It transitions your interest from a casual viewing to a serious, protected legal claim on an asset.

The Legal Significance of the OTP

Singapore property law operates on the principle of “Offer and Acceptance.” A verbal agreement or a handshake is never enough in this market. Without a signed OTP and a paid fee, you have no legal standing. The OTP acts as a unilateral contract. The seller is bound to sell, but you, the buyer, have the choice to walk away. If you don’t exercise the option, you lose the fee, but you aren’t forced to complete the purchase. This differs from a Sale and Purchase Agreement (S&P), which is the final contract that binds both parties to the completion of the sale.

Key Stakeholders Involved in the OTP Process

Mastering the OTP stage requires coordinating with several key players. Your property agent handles the initial negotiation and ensures the OTP form is filled out correctly. Your conveyancing lawyer is equally vital. They’ll review the terms to protect your interests and manage the “exercise” process later.

- The Grantor: The seller who grants the right to buy.

- The Grantee: You, the investor, who holds the right.

- The Bank: Your lender must provide a Letter of Offer (LO).

Timing is everything. You must secure your bank’s Letter of Offer before the OTP expires. If you exercise the option to purchase without a confirmed loan, you risk losing your 5% deposit if your financing falls through. Smart investors always get their In-Principle Approval (IPA) before they even sign the OTP. This disciplined approach prevents expensive mistakes and ensures your path to asset progression stays on track. To maximize your borrowing power and secure the most competitive rates, it pays to find a mortgage broker in Singapore who can act as a strategic financing partner before you commit to any deal.

HDB vs. Private Property: Navigating the Different OTP Rules

Successful asset progression in Singapore requires a deep understanding of how the option to purchase (OTP) functions across different asset classes. You can’t treat an HDB transaction the same way you treat a luxury condo or an industrial unit. The rules of engagement change the moment you switch from public to private markets. While HDB transactions follow a rigid, state-mandated path to ensure social stability, the private sector offers a playground for negotiation and strategic maneuvering. You must master these distinctions to protect your capital and secure the right deals without falling into common traps.

The HDB OTP Workflow

HDB transactions require absolute adherence to the HDB-prescribed form. You don’t have the luxury of drafting custom clauses. The process is strictly managed through the HDB Resale Portal. Sellers can only grant an OTP after they’ve officially registered their Intent to Sell for at least 7 days. Once the price is agreed upon, the buyer pays an Option Fee, which is a maximum of S$1,000.

- Valuation Timing: Buyers must apply for the HDB valuation within 1 working day after the OTP is granted if they intend to use CPF or a bank loan.

- The Cooling-off Period: HDB mandates a 21-day option period. This is a fixed window where the buyer decides whether to proceed. It can’t be shortened or extended through private agreement.

- Exercising the Option: To finalize, the buyer pays an Exercise Fee (usually S$4,000), ensuring the total deposit doesn’t exceed S$5,000. This entire workflow is tracked digitally, leaving zero room for procedural errors.

Private Property OTP Nuances

Private property offers the flexibility that seasoned investors crave. The seller’s lawyer usually drafts the document, meaning terms are often negotiable. While the standard industry practice is a 14-day option period, smart investors often negotiate for 21 or even 30 days. This extra time is crucial for finalizing high-leverage financing or conducting deeper due diligence on co-living conversions.

The financial structure is also more intensive. You’ll typically pay a 1% Option Fee to secure the property. To exercise the option, you must pay the remaining 4% Exercise Fee within the agreed timeframe, totaling a 5% cash outlay. Because these documents are private contracts, they can contain non-standard clauses regarding furniture, repairs, or specific vacant possession terms. Understanding the legal implications of an OTP is vital before you sign, as backing out usually means forfeiting that 1% deposit. If you want to master property investment strategies and avoid expensive mistakes, you must learn to audit these documents for “hidden” seller-friendly clauses that could jeopardize your cash flow. Precision at this stage separates the amateurs from the professional investors who consistently build wealth through the Singapore market.

The Investor’s Dilemma: What Happens if You Back Out?

Deciding to walk away from a deal is a heavy call. The most immediate consequence you face is the forfeiture of your Option Fee. For a typical S$1.5 million private property, that 1% fee equals S$15,000. It’s a painful hit to your capital, but seasoned investors know that losing 1% is better than being trapped in a S$1.5 million mistake. While sellers rarely sue for “Specific Performance” to force a residential sale, they legally hold the right to keep your deposit as liquidated damages. Most investors find themselves in this corner due to bank loan rejections, a low valuation, or sudden “buyer’s remorse” after seeing a better deal. Don’t let this be you. Secure an In-Principle Approval (IPA) from your bank before you ever sign the option to purchase. This single step eliminates the guesswork and confirms exactly how much the bank will lend you.

Understanding Forfeiture and Penalties

Losing S$10,000 or S$20,000 feels like a massive setback. However, you must weigh this 1% loss against the risk of a bad investment that bleeds cash every month. If the property’s potential for positive cash flow disappears because of a high interest rate, walking away is a strategic retreat. If the seller is the one who backs out after signing, the rules change. They must refund your Option Fee in full. In many cases, you may even seek legal damages if the contract was breached. Protect your “earnest money” by engaging a sharp conveyancing lawyer early. They ensure the contract terms don’t leave you vulnerable if the seller gets a higher offer from someone else.

The ‘Subject to Financing’ Clause

You might hear about a “Subject to Financing” clause, which lets you cancel the deal if your loan fails. In the competitive Singapore market, this clause is incredibly rare. Sellers want certainty. If you demand this condition, most sellers will simply move to the next buyer in line. You must mitigate your risks before the 14-day window closes. Check your valuations with at least three different lenders to ensure the bank’s numbers match your offer price. The Option Period serves as a critical 14-day safety net that allows investors to finalize their financial calculations and confirm bank support before committing to the full purchase price. Use this time to verify your TDSR limits and ensure your cash reserves are ready for the 4% exercise fee. Knowing how to find a mortgage broker who specializes in investor financing can be the difference between a smooth loan approval and a costly forfeiture. Master these steps, and you’ll navigate the option to purchase with the confidence of a pro.

Step-by-Step: From Viewing the Property to Exercising the OTP

Mastering the property acquisition process requires a disciplined approach. You don’t want to leave your investment to chance. Follow this systematic blueprint to secure your option to purchase without the stress of missed deadlines or legal hiccups.

- Step 1: Negotiation. After viewing the property, agree on the purchase price. Don’t rush this; ensure the numbers align with your high-yield strategy and cash flow projections.

- Step 2: Option Fee. Pay the Option Fee to the seller. For private properties, this is typically 1% of the purchase price. For HDB flats, it is a negotiated amount not exceeding S$1,000. In exchange, you receive the signed OTP document.

- Step 3: The Option Period. This is your window for final checks. You must secure your bank loan and engage a conveyancing lawyer immediately.

- Step 4: Exercise the Option. Sign the Acceptance Copy and pay the Exercise Fee. For private property, this is usually 4% of the price. For HDB, the total of the Option Fee and Exercise Fee cannot exceed S$5,000.

- Step 5: Completion. Your lawyer handles the stamping and legal transfer. This process typically concludes within 8 to 12 weeks from the date you exercise the option.

The Critical 14-21 Day Window

Time is your greatest asset or your biggest risk. Private property transactions usually allow a 14-day window; HDB grants 21 days. You must act fast. If you miss the deadline, the seller keeps your Option Fee and the deal dies. Use this checklist to stay on track:

- Order a formal valuation to ensure your loan covers the purchase price.

- Finalize your Letter of Offer (LO) with your mortgage broker.

- Appoint a lawyer to begin title searches and due diligence.

Don’t wait until day 10 to talk to your bank. Lenders often take 3 to 5 business days to process a Letter of Offer. A delay here is an expensive mistake you can’t afford.

Due Diligence During the Option Period

Investors must look beyond the aesthetics. Verify property boundaries and look for unauthorized alterations like illegal mezzanine floors or hacked structural walls. These can lead to heavy fines from the Building and Construction Authority (BCA). Review the Inventory List carefully. Ensure the air-conditioning units and kitchen appliances mentioned in the deal are actually staying. Whether you are comparing HDB vs Condo for your next move, your due diligence remains the same: protect your capital at all costs. Once you’ve successfully acquired the property, you’ll need to prepare for the next phase of your investment journey by understanding how to structure a comprehensive tenancy agreement Singapore that protects your rental yield and minimizes legal risks.

Ready to build a portfolio that generates consistent passive income? Join our next masterclass to learn the proven blueprint for Singapore property success.

Mastering the OTP Stage with Proptiply’s Proven Framework

Understanding the technicalities of a document is only half the battle. To truly succeed in the Singapore property market, you need to transition from a passive reader to a savvy executor. Our Residential Acceleration Program is designed to bridge this gap. We teach you how to identify “undervalued” deals long before the option to purchase is even drafted. By analyzing historical transaction data and current rental yields, our students learn to spot properties priced 5% to 10% below market value, ensuring equity is built from day one.

Success requires a fundamental shift from the “Homebuyer Mindset” to the “Investor Mindset.” While a homebuyer might get distracted by a unit’s aesthetic or the view from the balcony, an investor focuses strictly on the numbers. When you sign an option to purchase, you aren’t just buying a house; you’re acquiring a cash-generating asset. We train you to look past the staging and focus on the floor plan efficiency and the potential for asset progression. Once you’ve secured your property through the OTP process, the next critical step is protecting your investment returns through a properly structured tenancy agreement Singapore that safeguards your rental income and minimizes tenant-related risks.

One of the biggest fears for new investors is the “valuation gap.” This happens when the bank’s valuation comes in lower than your purchase price, forcing you to pay the difference in cash or risk losing your deposit. Proptiply students rarely face this issue. We teach a rigorous pre-purchase protocol that involves getting indicative valuations from at least three major banks before any money changes hands. This disciplined approach transforms property acquisition from a gamble into a calculated business move.

Avoid Expensive Mistakes with Expert Guidance

Precision is everything in real estate. That’s why we offer a 1-on-1 Property Portfolio Consultation to help you review your entry price and financial standing. Our mentors have seen it all. In one instance, a mentor helped a student negotiate a S$25,000 reduction in the asking price by identifying specific maintenance issues that the seller hadn’t disclosed. This level of “boots-on-the-ground” experience is what prevents beginners from overpaying in a competitive market. Professional education serves as the ultimate insurance policy against the risk of losing your 1% option fee due to lack of market data.

Ready to Start Your Investment Journey?

Don’t let the complexity of Singapore’s property regulations hold you back from financial freedom. We invite you to join our next property investment bootcamp, where we deconstruct the entire acquisition process. Our community provides the “insider knowledge” you won’t find in news reports, such as how upcoming changes in the URA Master Plan will impact specific districts like Jurong Lake District or the Greater Southern Waterfront. It’s time to stop guessing and start building your multi-property portfolio with a tested blueprint.

Master Your Property Acquisition with Confidence

Navigating the option to purchase is more than a formality; it’s a strategic move that requires precision. You’ve learned that HDB regulations cap option fees at S$1,000, while private transactions typically demand a 1% fee that you risk losing if you hesitate. Avoid expensive mistakes by following a disciplined timeline from viewing to exercise. Success in the Singapore market isn’t about luck. It’s about applying a proven framework that protects your capital and secures high-yield assets.

Don’t leave your financial future to chance. Founders Jelene Lum and Ervin Ang have built a legacy on mastering high-yield niches like co-living and industrial spaces. They’ve already paved the way, and now they’re ready to share the blueprint with you. You’ll get more than just theory; you’ll receive a personalized 1-on-1 consultation to craft your bespoke investment roadmap. Take the first step toward building a portfolio that generates consistent passive income today.

Secure Your Investment Future: Join the Residential Acceleration Program

Your journey toward a robust property portfolio starts with a single, informed decision. The path to financial freedom is open to those who take action, and we’re here to guide you every step of the way.

Frequently Asked Questions

Can I negotiate the length of the Option to Purchase period in Singapore?

You can absolutely negotiate the length of the option to purchase period with the seller to suit your timeline. While the standard duration is 14 days for private residential properties, savvy investors often request 21 days or more to secure their financing. For HDB flats, the option period is fixed at 21 days according to HDB regulations and cannot be extended. Always ensure any agreed extension is documented in writing before you pay the option fee.

What is the difference between an Option Fee and an Exercise Fee?

The Option Fee is the initial payment, typically 1% of the purchase price, that grants you the exclusive right to buy the property. In contrast, the Exercise Fee is the amount paid when you officially sign the document to commit to the deal, usually 4% for private properties. Together, these sums form the 5% cash downpayment required under standard Singapore property sale terms. Master these numbers early to ensure your cash flow is ready for the transaction.

Is the Option to Purchase legally binding if I haven’t signed the Sales and Purchase agreement yet?

An option to purchase becomes a legally binding contract the moment the seller signs it and accepts your option fee. Although you haven’t signed the formal Sale and Purchase Agreement yet, the seller is legally prohibited from offering the property to anyone else during the option period. If you fail to exercise the option, you’ll forfeit the option fee, which is usually 1% of the agreed price. This protects your interests while you finalize your mortgage arrangements.

What happens if my bank loan is rejected after I’ve already paid the Option Fee?

If your bank loan is rejected, you’ll typically forfeit the 1% option fee you’ve already paid to the seller. Most standard agreements in Singapore don’t include a “subject to loan” clause, so you must secure an In-Principle Approval (IPA) before handing over any cash. To avoid this expensive mistake, always ensure your finances are airtight before committing to a deal. Our blueprint for success always starts with a clear understanding of your borrowing capacity.

Can a seller cancel the OTP after granting it to me?

A seller cannot cancel the OTP once they’ve signed the document and accepted your option fee. The law protects you as the buyer, giving you the exclusive right to purchase the property within the specified timeframe. If a seller tries to back out, you can seek legal recourse to enforce the contract or claim damages. This certainty is why the OTP is a critical tool for securing your next investment and building your portfolio.

Do I need a lawyer to sign the Option to Purchase?

You don’t need a lawyer to physically sign the initial OTP, but you must engage one immediately after to handle the conveyancing process. Your lawyer will perform necessary title searches and manage the legal transfer of ownership once you decide to exercise the option. For private properties, the law requires a qualified solicitor to witness your signature on the instrument of transfer and coordinate with the Singapore Land Authority. Professional legal guidance helps you avoid hidden pitfalls.

How much is the Buyer’s Stamp Duty (BSD) and when must it be paid during the OTP process?

Buyer’s Stamp Duty (BSD) is calculated based on the property’s purchase price, with rates reaching 6% for portions exceeding S$3,000,000. You must pay this tax to IRAS within 14 days of exercising your option. Failing to meet this deadline results in heavy penalties, so you must budget for this cost alongside your initial downpayment. This is a non-negotiable expense that every serious investor must factor into their asset progression strategy.

Can I transfer my Option to Purchase to another person (Nominee clause)?

You can transfer your right to purchase if the OTP includes an “and/or nominee” clause. This allows you to nominate another person or a corporate entity to take over the contract before it’s exercised. However, HDB regulations strictly prohibit nomination, so this strategy only applies to private residential or commercial properties in Singapore. Always confirm this clause is present if you plan to structure the deal through a different investment vehicle later.